Enterprises and government agencies the world over are busy changing gears these days. Large global publicly-owned commercial firms are seeking to get more agile and nimble. Small, often family-owned, private businesses are trying to become more mature to cater for growth whilst remaining responsive. Public sector organisations, to the extent they can, are trying to deliver outcomes for citizens faster. Speed, it seems, has become a number 1 issue for everyone. Cost and quality are definitely the next priorities but going quickly is a huge imperative.

The changes required are profound. The world outside organisations – particularly those using the products and services they provide – want new and improved offerings all the time. The world itself is changing at an unprecedented rate. Just keeping up with the demand for change – in many ways: socially, economically, technologically and practically – is mind boggling. The changes inside most organisations are lagging these external changes. It often requires “changing gears” to get the traction required to meet the challenge. Sometimes these gear-changes require new leadership. More often they need new approaches: updated methods, different skills, outside help and most importantly a fresh perspective.

Big multi-national organisations like international corporations find this very challenging. The successful ones with long track records of growth in many markets and many products or services are employing “rebalancing”. Euphemistically, this often means shifting focus from things that are not growing to newer things with growth potential. Smaller companies who’ve historically done one or two things well often get into other lines of business. Government agencies employ “reforms” – either a different way of doing the same thing or augmenting existing functions with additional responsibilities. The growth of public-private partnerships all over the world is a great example.

Technological change is both a driver and an enabler of changing gears. The relentless shift to providing on-line channels between producers and consumers has ramped up in recent times. You can see it in the high street shops. There are now less bookstores, music shops and video libraries. There are more cafes, restaurants and boutiques. The supermarkets and especially department stores are being replaced by petrol stations with convenience stores and fast-food outlets. Books, music and video content have shifted online the most. Business-to-consumer electronic commerce has been eating away at retailers at an ever-accelerating rate. People sit in cafes with their mobile devices for a few minutes then do their everyday shopping while they pay for fuel. Even paying for things has become more and more technically enabled: PIN & chip cards, tap-and-go cards and in a few cases using your smartphone. At one bank here in Australia, even the ATM allows you to transact with your smartphone app rather than the ATM itself.

All of these things have emerged to save people time. Yet all of these changes in the community involve even greater changes on the organisations serving the public. They revolve around speed-to-market and cost-to-delivery for many. For others, it involves participating in business-to-business electronic commerce, often alongside competitors. Employees increasingly work from home at least some of the time in an increasingly casualised relationship with their employer. People collaborate across borders, timezones and organisations in evermore virtual ways. Manufacturing and agriculture, already impressively automated in the developed world, is moving to new and different geographies supplying a more globalised marketplace. In Kenya, more people and small businesses use virtual banking and finance than real accounts with physical financial institutions. Microfinance is similarly prevalent in the developing world.

Many organisations do not make the change. Some get acquired by larger firms rather than attempting the change. Many go out of business before they can change. Some larger publicly-listed companies become privately-held in order to make the changes necessary which can be a very severe form of changing gears. Traditional media is severely under threat from new and social media. Governments continually shift expenditure priorities from physical services to e-government services. Taxation agencies are particularly noticeable in this space. On the other side of the spectrum, postal agencies are shrinking in response to diminished use of ‘snail-mail’. All of these forms of transformation are accelerating in step with the demand for newer and often more digital offerings. Even large-scale philanthropy – the so-called “philanthrocapitalism” – employs modern and very digital ways and means of supporting their causes.

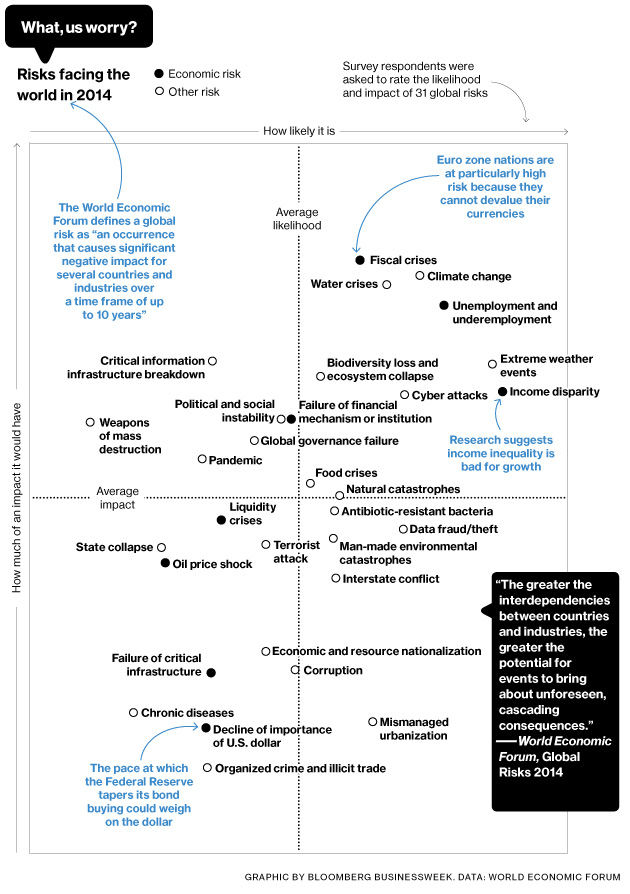

Yet most of the world’s people remain remarkably untouched by these titanic forces. “Only” a third of the world’s people are connected to the Internet. Half of humanity, mostly in the developing world, do not live in an urban area. Wealth and income have become concentrated among the rich few at a level not seen for a century. Education and employment opportunity still elude many. National, provincial and local tax revenues are being impacted by the sleepless world of transnational money in tax-havens and other arrangements. Capital markets have become “irrationally exuberant” again. But most people, two-thirds of humankind by some estimates, only ever see this on television.

It is true that globalisation and economic rationalism has brought great benefits to the world at large. Over the last thirty years, billions of people have been raised out of poverty because of it. But it’s also true that many have been left behind – and not only in the developing world. In the advanced nations, the middle class and older people have borne the brunt of the wealthiest becoming more wealthy. Corrupt and oligarchical minorities have benefitted at the expense of the majority in emerging countries. The numbers of poor across the world are dropping proportionally but increasing nominally. The global environment has also been impacted enormously.

Perhaps the greatest gear-change required is not so much within organisations, although they are certainly needed. The big gear-change is towards a more holistic perspective and a more inclusive one. Climate-change denial needs to become more akin to Holocaust denial: a criminal offence in some jurisdictions and certainly unacceptable behaviour elsewhere. War and terrorism similarly can’t go on the way it has been for the last few decades. Income and wealth inequality needs to be addressed before it becomes a trigger for unrest again. A new perspective is needed: one that considers the global impacts of an increasingly globalised world. We in the developed world have an historic opportunity to lead here. I hope we find the gear-lever to make the change in time…