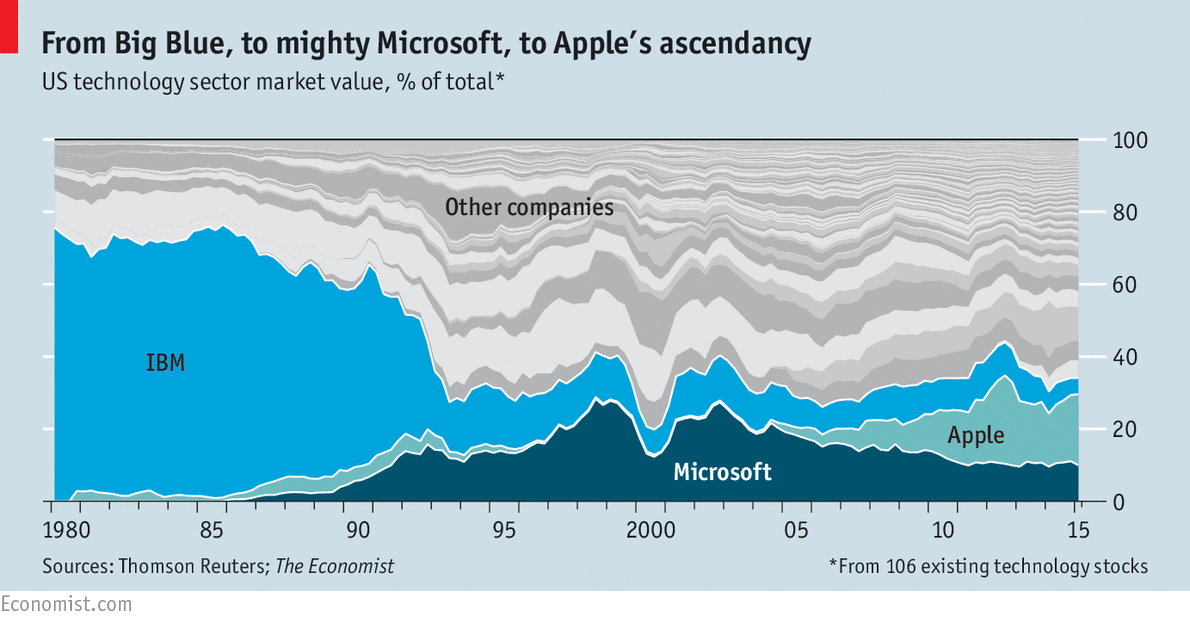

Apple is now part of the Dow Jones Industrial Average index, today replacing AT&T. It’s reminiscent of when Microsoft and Intel were added to the Dow in 1999. The changes in the share of market capitalisation over the last 30 years shows this clearly:

These changes reveal a central truth in the technology world. It has emerged from a decade of tumultuous change so that no one firm – or its way of providing technology is dominant. The ramifications are far-reaching. Platform plurality is back. Competition is severe. Continuous delivery of incrementally new and improved devices and services are required. Most of all, business models have changed.

These changes reveal a central truth in the technology world. It has emerged from a decade of tumultuous change so that no one firm – or its way of providing technology is dominant. The ramifications are far-reaching. Platform plurality is back. Competition is severe. Continuous delivery of incrementally new and improved devices and services are required. Most of all, business models have changed.

This is indicative of what Carlota Perez calls “Phase 4”, or ‘Maturity’ in her long-cycle economic model:

It is a commoditised and largely consumer-oriented form of what used to be proprietary and expensive enterprise-oriented technology. The cell-phone was, ironically, invented in the 1940s by AT&T (Bell Labs). Early cell-phones of the 1980s were expensive and cumbersome business-only tools. Today, an iPhone connected over the public wireless broadband networks can often be more useful than a desktop PC connected over an enterprise’s network and an old cellular “dumb phone” put together . There are more apps, more services, more data and more continuously delivered new functionality than could ever be expected from a company’s (or Government department’s) IT group. The ecosystems have scaled outside the house and onto the streets for everyday ordinary people.

The leading firms have made extraordinary investments over the last decade or so. The business models that fuel these investments are as varied as they can be: Apple does it by profitable sales of devices, Google does it through advertising, Microsoft does it by reinvesting profits from Windows and Office into Cloud data centres and directly making devices, Amazon does it by reinvesting retail surpluses into Amazon Web Services, Facebook does it by selling data about people to marketeers. Regardless of how, the raison d’etre is growth, reach, and most importantly, building a deep ecosystem.

Apple’s ecosystem efforts started in music with the iPod and iTunes over a decade ago. From this base, they projected forward into video content with the Apple TV set-top box. Then came the iPhone which extended the ecosystem into apps. The iPad broadened this into publishing and now the Watch into wearables. The genius of Apple’s ecosystem is its potential for lock-in. The loyalty of the customer base and their unprecedented high levels of satisfaction with the products is a hallmark of Apple’s success.

Google’s ecosystem has trailed Apple’s. If anything, it has been emulating Apple’s approach in more recent times. Controversially, the Android phone platform and the Google Play app store bear more than a striking resemblance to the corresponding pieces of the Apple ecosystem. Google is different in that they don’t make devices and have much lower pricing, which appeals to a broader audience and a far less profitable business model. Their leading device manufacturer Samsung has recently struggled to keep up with Apple’s more vertically-integrated and more profitable model.

Microsoft’s ecosystem has changed dramatically in the last few years. They were renown for being a software-oriented hub of a vast ecosystem of hardware makers with a huge number of business partners. Now Microsoft directly makes phones and has tablets and Cloud servers made for them directly. The latest version of their Surface Pro tablet-cum-PC has sold well. Their Cloud business is growing nicely. Their Lumia smartphones have fared dismally against Apple’s iPhones and the more dominant Android smartphones.

Facebook has a very different kind of ecosystem. At the most basic level, they’ve open sourced the technology of their data centres in the Open Compute project. Something similar is underway in their communications technology. People are adopting Facebook’s infrastructure designs and implementations as a cost-effective way of embracing the Cloud. Facebook has an app ecosystem and an advertising ecosystem too. But in terms of social networking they are head and shoulders above everyone else with almost a billion-and-a-half average monthly users.

Amazon has focussed on selling commodity Cloud infrastructure to a wide variety of customers. Mostly, it’s a pay-as-you-go public Cloud offering. However, more recently, especially in Government, they are making private Clouds. The most famous is the one at the CIA – completely isolated. GovCloud is a shared offering for US Government-only clients. They are starting to enter the world of hybrid Clouds by way of interfacing technologies. Their ecosystem consists of a marketplace of solutions to run in the Amazon Cloud, some partner organisations along the legacy Microsoft model and a few other things.

IBM’s entry into the Cloud, Mobile, Social and Big Data worlds has been belated but successful. They bought SoftLayer and placed on top of it BlueMix. They’ve partnered with Apple on enterprise apps for iOS. Twitter has partnered with IBM for enterprise social networking. But IBM’s big data offering is a natural extension of what it’s been doing in analytics for decades. The ecosystem is unclear and significantly fragmented at the moment. It is clearly a work-in-progress that may take years to complete. Meanwhile, old-IBM is struggling.

These changes – from PCs to smartphones, from servers to Clouds, from email & chat to social networking, from decision support systems to Big Data analytics – are profound. They have already changed the world. They will continue to do so in ways that we probably can’t yet envisage. Wearables like the Apple Watch are already disrupting the watch business. Today, LVMH’s Tag Heuer announced a partnership with Google and Intel to produce a Tag connected watch. Never thought I’d see that in my lifetime!